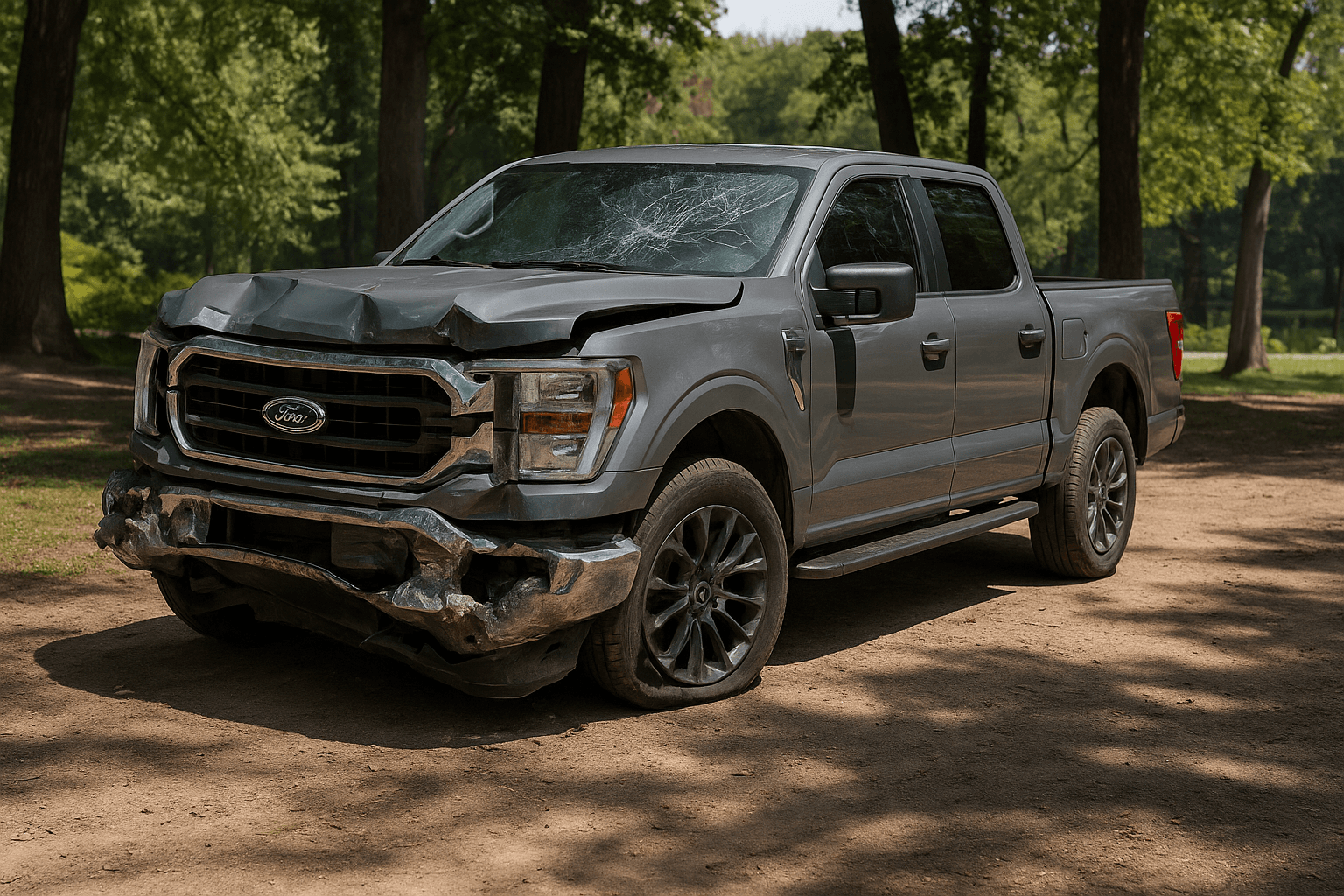

Your vehicle was totaled while you're carrying FR-44 insurance in Florida. Your FR-44 filing doesn't automatically transfer to a replacement vehicle, and a coverage gap of even one day triggers state notification and license suspension.

Your FR-44 filing stays with the policy, not the driver — and the clock just started

Florida's FR-44 requirement attaches to your insurance policy, not to you as a driver. When your vehicle is totaled and that policy ends, your FR-44 coverage ends with it, even though your underlying DUI conviction still requires continuous FR-44 filing for the full three-year compliance period measured from your reinstatement date.

The Florida Department of Highway Safety and Motor Vehicles receives automatic SR-26 notification from your carrier the day your policy lapses. That notification triggers immediate license suspension. There is no grace period for vehicle shopping, no administrative window while you're comparing replacement options, no exemption because the lapse was caused by a total loss rather than non-payment.

Most seniors assume they have reasonable time to replace a totaled vehicle before addressing insurance. Under FR-44, that assumption costs you your license. The filing must transfer to replacement coverage before your current policy cancels, which typically happens 30 days after the total loss settlement if you don't replace the vehicle on that policy.

What happens to your current FR-44 policy after the total loss settlement

Your carrier pays the actual cash value of your totaled vehicle and removes it from your policy. If that was your only insured vehicle, the policy cancels 30 days after settlement unless you add a replacement vehicle. If you carried collision and comprehensive coverage, the settlement check arrives within 7-10 business days in most cases. The FR-44 filing remains active during those 30 days only if the policy itself remains active.

Seniors often use that 30-day window to shop carefully for a replacement vehicle, comparing options and arranging financing if needed. That's reasonable financial planning for a standard auto policy. Under FR-44, it's a compliance violation. Your license suspends the day after your policy cancels, even if you're mid-negotiation on a replacement vehicle.

If you carried liability-only coverage on an older vehicle — common among seniors on fixed incomes — you received no settlement check, but the compliance timeline is identical. The policy cancels when you notify your carrier the vehicle is no longer drivable, or when they learn of the total loss through other channels. You have until that cancellation date to secure replacement FR-44 coverage.

Get FR-44 insurance quotes from carriers that file in Florida and Virginia

FR-44 requires higher liability limits than SR-22 — compare carriers that understand the difference.

Get Your Free Quote✓ FR-44 Filing Included✓ No Obligation✓ Licensed Carriers✓ FL & VA Specialists

Your three options to maintain continuous FR-44 compliance after a total loss

Option one: Add a replacement vehicle to your existing FR-44 policy before the totaled vehicle is removed. This maintains continuous coverage with no lapse and no SR-26 notification to the state. You'll need the VIN, make, model, and year of the replacement vehicle. Your carrier re-rates the policy based on the new vehicle, typically within 24 hours. If you're replacing a 2008 sedan with a 2020 SUV, expect a significant premium increase — the FR-44 filing fee stays the same, but collision and comprehensive costs rise with vehicle value.

Option two: Purchase a non-owner FR-44 policy immediately after your vehicle policy cancels. Non-owner policies provide liability coverage when you're driving a vehicle you don't own — a rental, a borrowed vehicle, or a vehicle you're test-driving before purchase. Florida allows non-owner FR-44 policies to satisfy the state filing requirement during gaps in vehicle ownership. Premium for non-owner FR-44 typically runs $125-$200 per month with the same 100/300/50 liability minimums required for vehicle policies. Not all carriers offer non-owner FR-44 — Bristol West, Direct Auto, and Dairyland write them in Florida; State Farm and Geico typically do not.

Option three: If another household member owns a vehicle and maintains their own policy, add yourself as a listed driver on that policy and request FR-44 filing on it. This works if you're living with an adult child or spouse who has their own insured vehicle. The FR-44 filing attaches to their policy, raising their premium substantially — typically $800-$1,200 annually for the filing alone, plus the increased liability limits if their current policy carries less than Florida's 100/300/50 FR-44 minimum. Most family members are willing to help temporarily, but few anticipate the cost impact. Discuss the premium increase before requesting the filing.

The reinstatement process if your license suspends during the vehicle replacement gap

If your FR-44 policy lapses before you secure replacement coverage, Florida DMV suspends your license the day after receiving SR-26 notification from your carrier. That suspension remains in effect until you file proof of new FR-44 coverage and pay reinstatement fees. The reinstatement fee for FR-44 lapse is $150 for the first offense, $250 for a second lapse, and $500 for a third lapse during your three-year compliance period, plus a $45 service fee.

You cannot reinstate online. You must visit a Florida driver license office in person with your new FR-44 certificate, proof of identity, and payment. Current wait times at most Florida DHSMV offices run 60-90 minutes even with an appointment. Some metro offices (Miami-Dade, Broward, Orange County) run longer. Your new FR-44 policy must be active before you visit — the filing transmits electronically to the state, but processing takes 24-48 hours. Plan for a three-day gap between purchasing new coverage and license reinstatement.

Driving during suspension — even to the DMV office for reinstatement, even in an emergency — adds a second-degree misdemeanor charge carrying up to 60 days in jail and a $500 fine. Seniors often assume a suspended license for administrative reasons rather than DUI allows limited driving. Florida law makes no distinction. Arrange a ride or use rideshare for your reinstatement appointment.

How total loss affects your FR-44 premium when you replace the vehicle

FR-44 premium has two components: the liability coverage cost based on your driving record and the FR-44 filing fee. The filing fee stays constant regardless of vehicle — typically $25-$50 annually depending on carrier. The liability premium, however, re-rates every time you change vehicles, and seniors replacing a totaled older vehicle with a newer one typically see significant increases.

A 68-year-old Florida driver carrying FR-44 on a paid-off 2010 Honda Accord with liability-only coverage might pay $240 per month. Replace that Accord with a 2019 Honda CR-V requiring collision and comprehensive under a loan agreement, and the same driver now pays $420 per month for the same FR-44 filing. The filing requirement didn't change. The vehicle value, repair costs, and theft risk changed.

Non-standard carriers price FR-44 coverage 2-3x higher than standard market rates. That multiplier applies to the full premium, not just the filing fee. Seniors shopping for a replacement vehicle while under FR-44 should calculate insurance cost before finalizing the purchase. A $15,000 vehicle requiring full coverage might cost $5,000 annually to insure under FR-44 — one-third of the vehicle's value every year. For seniors on fixed retirement income, that math often forces a choice of a less expensive replacement vehicle than they'd prefer.

Why most major carriers non-renew FR-44 policies after total loss claims

State Farm, Geico, Allstate, and Progressive typically file FR-44 for existing customers who receive a DUI conviction during an active policy term. They're less willing to continue that filing through a total loss claim and vehicle replacement. Non-renewal notices arrive 45-60 days before your policy term ends, giving you time to secure replacement coverage. After a total loss claim, many carriers accelerate that timeline.

The non-renewal isn't punitive. Carriers price FR-44 filings as high-risk, but they price them within standard-market underwriting guidelines because you were already a customer when the conviction occurred. When you file a total loss claim, underwriting re-evaluates your risk. A DUI conviction plus a total loss claim — regardless of fault — triggers non-renewal at most major carriers. You'll complete your current policy term, but you're moving to the non-standard market at renewal.

Bristol West, Direct Auto, Dairyland, GAINSCO, The General, Safe Auto, Acceptance, and Mendota specialize in FR-44 coverage and expect both DUI convictions and claims in their book of business. Their premiums are higher than major carriers, but they don't non-renew for claim activity the way standard market carriers do. Expect to pay $180-$320 per month for FR-44 coverage in Florida's non-standard market depending on age, vehicle, and coverage selections. That rate holds more stable through claims than major carrier pricing.

If you're not replacing the vehicle — can you suspend FR-44 until you buy again?

Florida does not allow FR-44 suspension during your three-year compliance period. The filing requirement runs continuously from your reinstatement date for exactly 36 months regardless of whether you own a vehicle, drive regularly, or move out of state temporarily. If you're not replacing your totaled vehicle immediately, your only compliant option is a non-owner FR-44 policy.

Some seniors assume they can simply not drive until they're ready to purchase a replacement vehicle, letting their license suspend without consequence because they're not using it. That assumption creates two problems. First, Florida assesses reinstatement fees and extends your FR-44 compliance period for every lapse. A 30-day gap costs $150 in fees and adds 30 days to the back end of your three-year requirement. Second, a suspended license complicates financial transactions beyond driving — loan applications, lease agreements, and some employment background checks flag license suspensions.

Non-owner FR-44 policies cost roughly half what vehicle policies cost because they carry no collision or comprehensive coverage. A Florida senior paying $280 per month for FR-44 on a 2015 sedan might pay $140 per month for non-owner FR-44 during a six-month period between vehicles. That's $840 for compliance alone, but it's cheaper than reinstatement fees plus the compliance period extension, and it keeps your license valid for non-driving purposes.