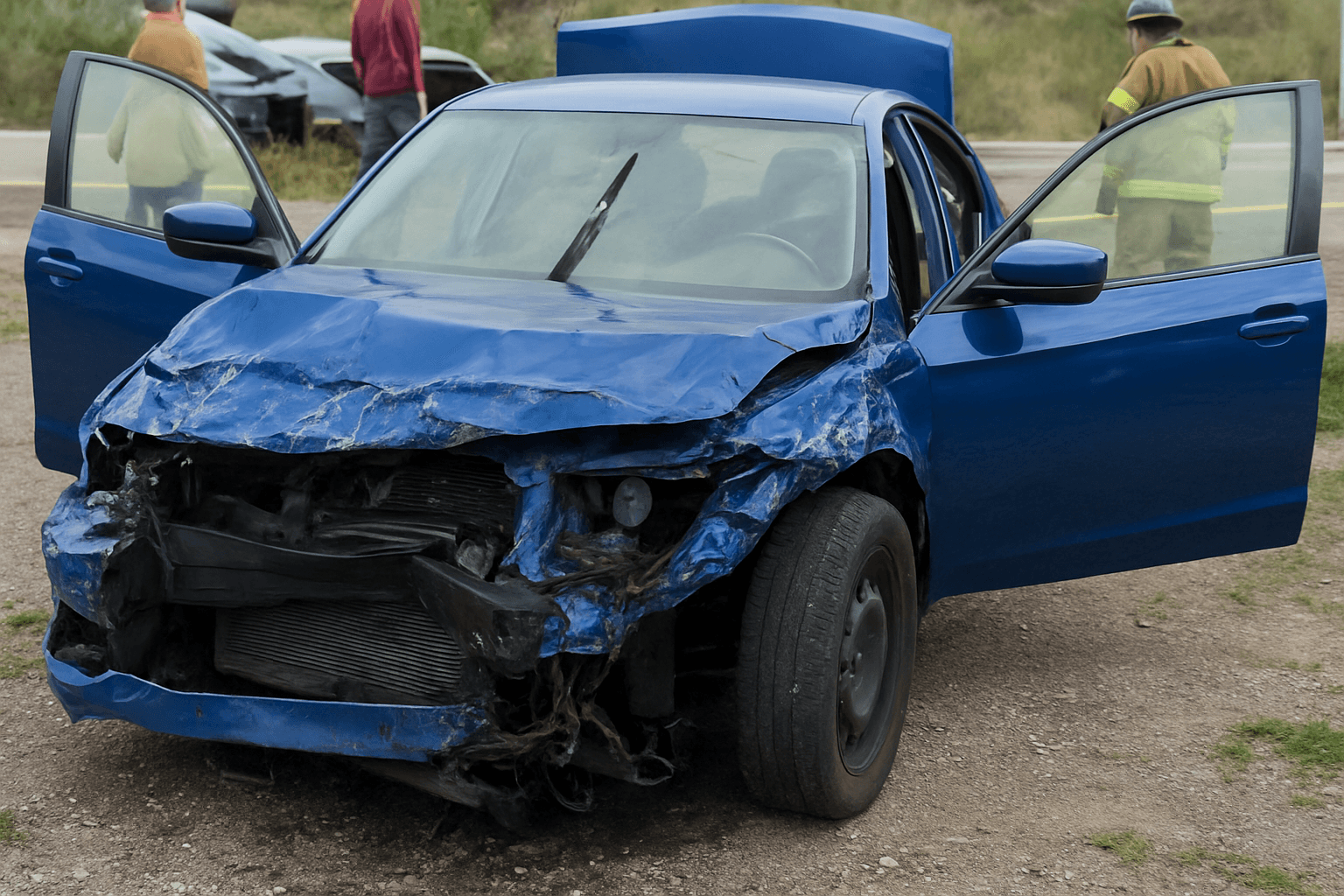

Property damage from a DUI conviction in Virginia triggers specific FR-44 filing requirements and affects both your court process timeline and DMV reinstatement. Here's what happens when the conviction includes property damage and how it changes your compliance path.

How Property Damage Affects Your Virginia DUI Case Timeline

A DUI conviction with property damage in Virginia follows the same criminal court timeline as a standard DUI — typically 30 to 90 days from arrest to conviction depending on whether you hire counsel and whether the case goes to trial. The property damage itself doesn't change the criminal timeline, but it creates a parallel civil liability issue that affects your insurance situation immediately.

Virginia law requires FR-44 filing for three years following any DUI conviction, measured from the conviction date. If your case involved property damage to another vehicle, fence, building, or other structure, the property owner or their insurer can file a civil claim against you separately from the criminal case. That civil exposure is what complicates FR-44 placement.

Most drivers assume the FR-44 requirement starts after sentencing, but carriers actually evaluate your eligibility the moment you apply. If there's an open property damage claim listed on your CLUE report or disclosed during underwriting, many non-standard carriers either decline coverage or require proof the claim is settled before issuing the policy. This creates a timing problem: you need the FR-44 to reinstate your license, but you can't get the FR-44 until the property claim closes.

What Happens to Your License While the Property Claim Is Pending

Virginia DMV suspends your license immediately following a DUI conviction. You have seven days from the conviction date to request a restricted license hearing, which requires proof of FR-44 coverage before the hearing date. If you can't secure FR-44 coverage because of the pending property claim, you cannot obtain the restricted license — even if you've enrolled in ASAP and paid all court fines.

The license remains suspended until you file FR-44 proof with DMV. Under current Virginia requirements, the FR-44 must show 50/100/40 minimum liability limits and remain active for the full three-year period. Missing the seven-day restricted license window doesn't end your eligibility — you can request a hearing later — but it extends the period you're driving on a fully suspended license.

If the property damage claim takes months to resolve, you're functionally stuck. The conviction triggers the FR-44 requirement, but the open claim blocks carrier approval. Some drivers in this situation attempt to settle the property claim out-of-pocket to close it faster, but that requires knowing the claim amount and having the cash available.

Get FR-44 insurance quotes from carriers that file in Florida and Virginia

FR-44 requires higher liability limits than SR-22 — compare carriers that understand the difference.

Get Your Free Quote✓ FR-44 Filing Included✓ No Obligation✓ Licensed Carriers✓ FL & VA Specialists

Which Carriers Will Write FR-44 With an Open Property Damage Claim

Most major carriers non-renew existing customers after a DUI conviction and won't write new FR-44 policies at all. State Farm, Geico, Allstate, and Progressive typically file FR-44 for current policyholders through the end of the policy term but decline renewal. That pushes you into the non-standard market: Bristol West, Direct Auto, Dairyland, GAINSCO, The General, Safe Auto, Acceptance, and Mendota.

Among non-standard carriers, underwriting rules for open property claims vary. GAINSCO and Bristol West typically require written proof the claim is closed — either a release letter from the claimant's insurer or a settlement agreement — before issuing the policy. Direct Auto and The General sometimes approve coverage with an open claim if the driver provides a signed statement acknowledging the claim and agrees to higher premiums, but approval isn't guaranteed.

Dairyland and Safe Auto occasionally approve FR-44 policies with pending property claims under $5,000 if the driver can show proof of ASAP enrollment and court compliance. Claims above $5,000 or claims involving injury in addition to property damage almost always result in a decline until the claim closes. Every carrier pulls your CLUE report during underwriting, so undisclosed claims result in automatic denial and complicate future applications.

How to Accelerate Property Claim Resolution to Get FR-44 Coverage Faster

The fastest path to FR-44 coverage is closing the property damage claim before applying for insurance. If you had liability coverage at the time of the DUI incident, your insurer handles the claim and pays up to your property damage limit. Contact your claims adjuster immediately after conviction and ask for a written timeline to close the claim. Most property-only claims close within 30 to 60 days if liability is clear and the repair estimate is undisputed.

If you didn't have insurance at the time of the incident, you're personally liable for the property damage. The property owner or their insurer will send a demand letter. Respond in writing within 10 days acknowledging receipt — silence can escalate the claim to court. If the damage amount is under $2,000 and you have the cash, settling directly and obtaining a signed release letter closes the claim immediately and clears the underwriting block.

For claims above $2,000 or disputed liability, consult an attorney before settling. Some property owners inflate damage estimates knowing DUI defendants are under time pressure to reinstate their license. An attorney can verify the repair estimate against actual market rates and negotiate a settlement that closes the claim without overpaying. Settling a $3,000 claim out-of-pocket to access FR-44 coverage is sometimes cheaper than the extra months of suspended license and associated costs.

What Happens If You Can't Close the Claim Before Your Court Deadline

Virginia courts typically impose license suspension as part of DUI sentencing, with the suspension running concurrent to the DMV administrative suspension. If your restricted license hearing is scheduled and you can't obtain FR-44 coverage because of the open claim, the hearing proceeds without you presenting proof of insurance — and the restricted license is denied.

You can request a second hearing once the claim closes and you secure FR-44 coverage, but the court doesn't extend deadlines based on carrier underwriting delays. The license remains fully suspended until you complete all reinstatement requirements: FR-44 filing, ASAP enrollment, ignition interlock installation if ordered, reinstatement fee payment, and restricted license approval.

Some drivers attempt to file SR-22 instead of FR-44, assuming it satisfies the court requirement. It does not. Virginia DUI convictions require FR-44 specifically — SR-22 is not accepted for license reinstatement. DMV rejects SR-22 filings for DUI cases, and the rejection restarts your compliance timeline. The only exception is if your DUI conviction occurred in another state and Virginia is processing it as an out-of-state conviction — in that case, SR-22 may be accepted depending on the originating state's requirement, but this is rare.

How Property Damage Affects Your FR-44 Premium During the Three-Year Period

FR-44 premiums in Virginia typically run two to three times standard rates, with monthly costs ranging from $180 to $350 depending on age, location, vehicle, and driving history. Property damage from the DUI incident adds another surcharge layer. Non-standard carriers apply a claims surcharge for the at-fault property damage in addition to the DUI surcharge, with the combined impact raising premiums an additional 20% to 40%.

The property damage surcharge remains on your policy for three to five years from the claim closure date, which often extends beyond the three-year FR-44 filing period. If the property claim closed in 2024 and your FR-44 period ends in 2027, you'll carry the property surcharge into 2027 or 2028 depending on carrier rules. That means your premium may not drop significantly even after the FR-44 requirement ends — you're still surcharged for the underlying claim.

Some non-standard carriers offer claim forgiveness programs after 24 months of continuous coverage without additional incidents, but eligibility requires on-time premium payment and no lapses during the FR-44 period. Missing a single payment triggers an SR-26 lapse notice to DMV, which suspends your license immediately and restarts the three-year FR-44 clock from the reinstatement date — not the original conviction date. Estimates based on available industry data; individual rates vary by driving history, vehicle, coverage selections, and location.